Economic outlook

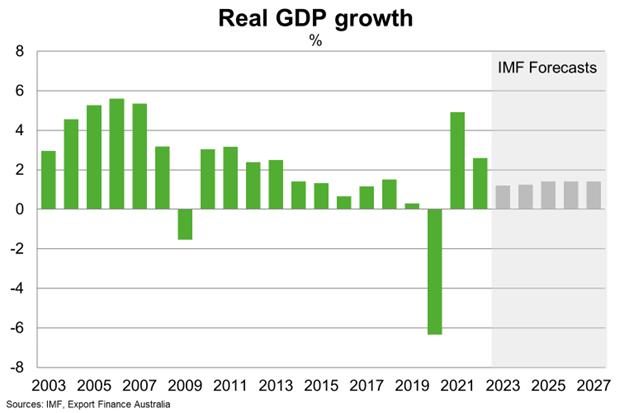

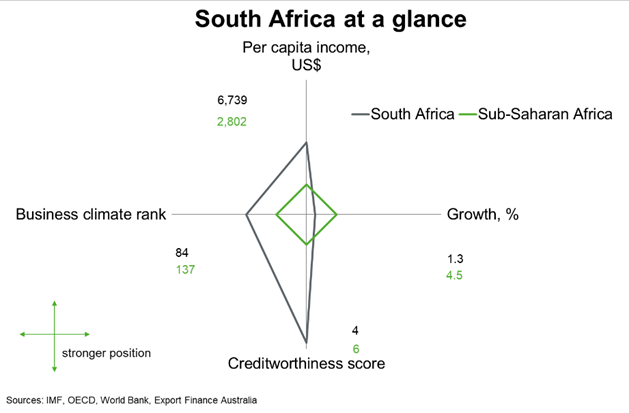

The lingering effects of the COVID-19 pandemic, flooding in Kwa-Zulu Natal, and widespread electricity cuts contributed to supply chain disruptions and damage to factories in 2022 that weakened an already fragile economy. South Africa’s economy grew 2.6% in 2022, slower than 4.9% in 2021.

The OECD forecasts real GDP to grow by just 1.2% in 2023. Private consumption and investment will continue to be the main drivers of growth. Household consumption will be supported by improving, albeit still weak, labour market conditions and social security transfer payments. Private investment will increase as companies replace an increasingly obsolete capital stock. On the downside, prices for South Africa’s key commodities are likely to fall in the short term, which alongside a slowing global economy, will weigh on export receipts.

Risks to the outlook include prolonged electricity shortages, a sharper global slowdown and more persistent high inflation that prompts faster monetary tightening than expected.

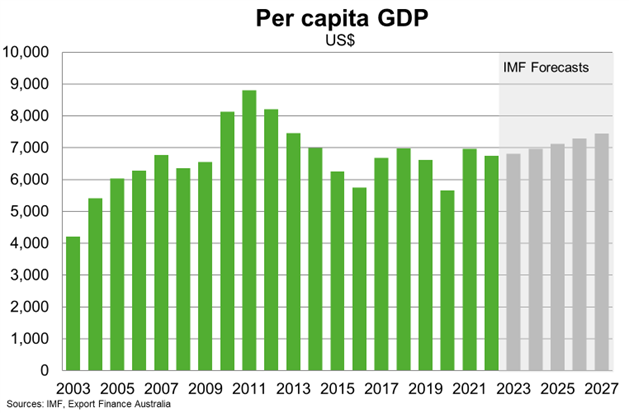

South Africa’s young population and location bode well for the long-term outlook, even in the face of a slowing birth rate. South Africa has better infrastructure than most other African countries. Moreover, the government has advanced several reforms, including for instance to combat corruption, to promote medium-term growth and fiscal consolidation. But long-standing economic, and financial social constraints, including large external imbalances, high public debt, intermittent energy supply, and heavy reliance on commodities are all likely to keep growth below 2% per annum in the medium term.